Welcome:

Login

|

Sign Up

|

About CircleID

Follow:

|

|

|

|

||

|

||

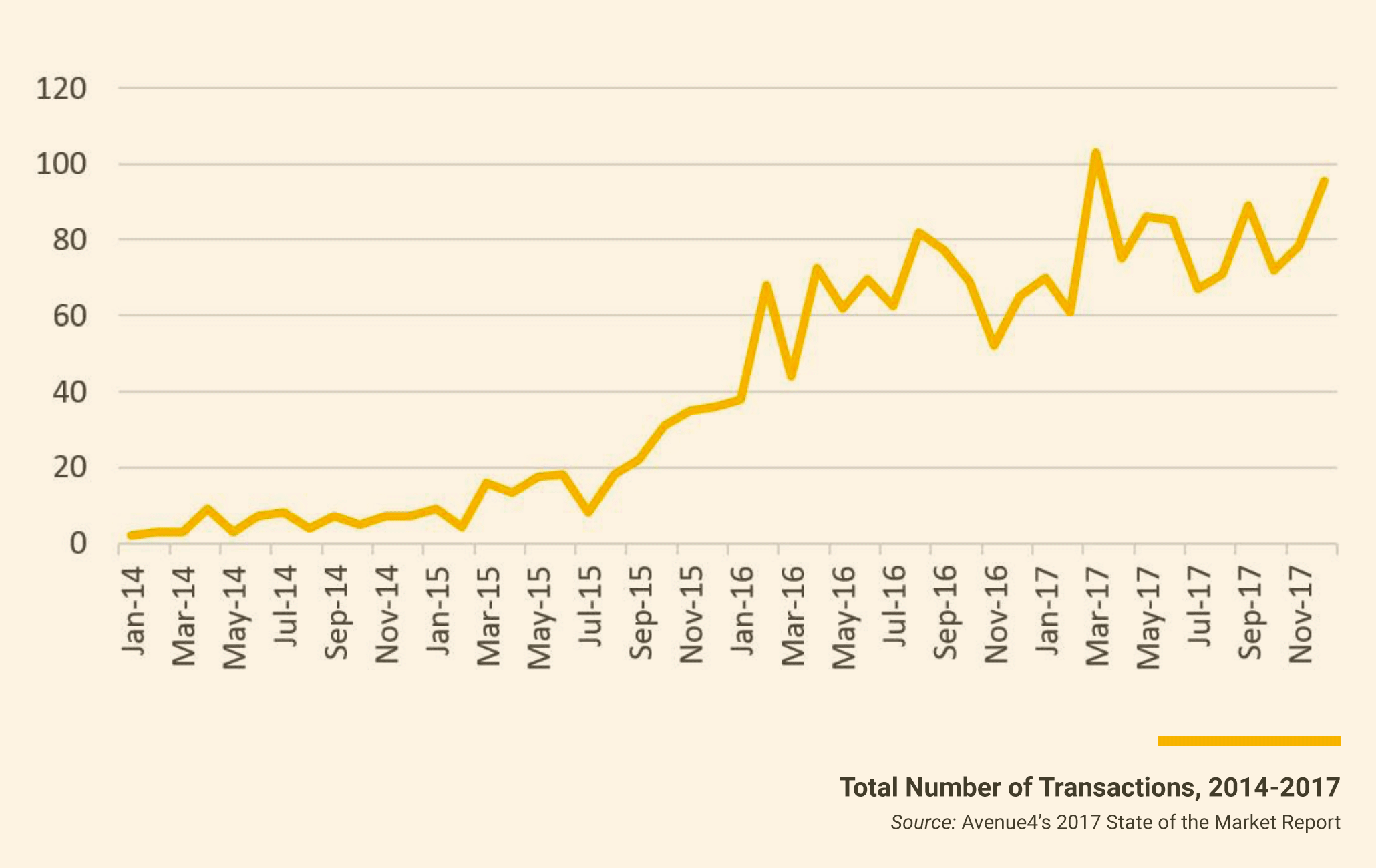

The IPv4 market has grown significantly in the last four years. It finished particularly strong in 2017, both in terms of the total volume of addresses traded and overall number of intra- and inter-RIR transactions in the ARIN region.

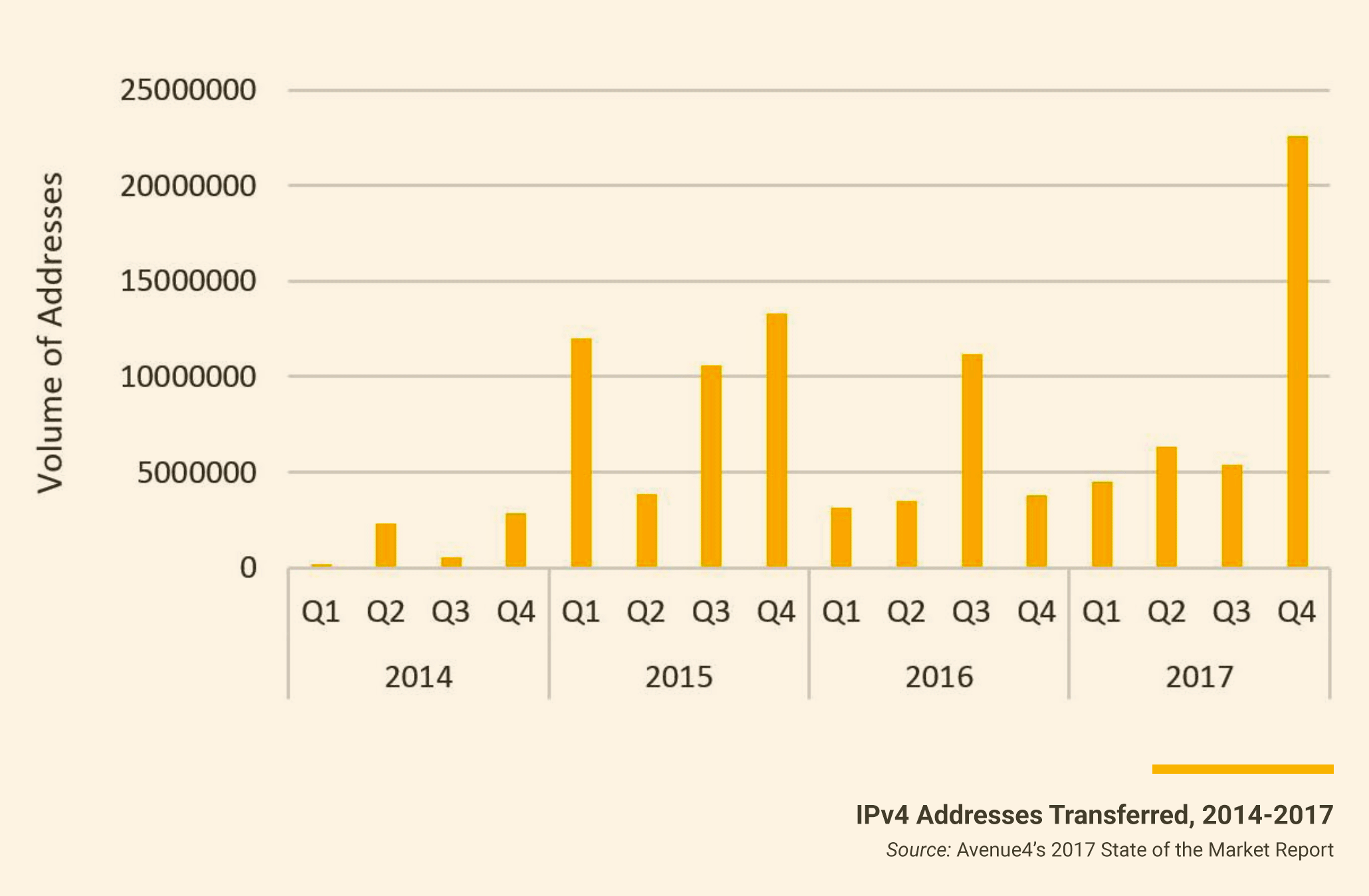

Over the last four years, the steady and sometimes substantial growth in the number of transactions has been mostly attributable to a dramatic increase in small block trades of fewer than 4,000 addresses. In contrast, the volume of addresses sold during the same period was much more volatile. Between 2014 and 2015, the volume of addresses traded increased seven-fold to nearly 40 million addresses. Between 2015 and 2016, this number dropped by half. Then between 2016 and 2017, the trading volumes skyrocketed again, more than doubling in the intra-RIR market. This pattern of activity is directly correlated to the dips and surges in available large block supply.

In our 2016 report, we attributed the sharp reduction in trading volumes to both the depletion of large block supply available in the marketplace, and the decision by some large block holders to delay entering the market altogether until large block pricing improved.

The 2017 rebound in part reflects the market’s response to this large block scarcity. Unit pricing for large block transactions has continued the steep upward trajectory that began at the end of 2016. Large blocks were trading for as little as $4 per number in 2015. By the end of 2017, they were trading for around $17-$18 per number—surpassing small block unit pricing for the first time. Heavily influenced by conditions in the large block market, unit pricing across the entire market has also climbed. In 2018, buyers should expect most informed sellers to set a floor price of $15 per number.

These escalating prices, in combination with increased buyer flexibility, prompted some new large block sellers to enter the market. Buyers are increasingly more willing to enter into contract structures that afford sellers more time to undertake renumbering efforts required to free up their supply.

Avenue4’s 2017 State of IPv4 Market Report – Analysis of the 2017 market and where it’s likely headed in 2018. (Download Report)In addition, large block buyers are more willing to accept smaller and smaller block sizes, which appeals to sellers that have substantial but fragmented unused address space. In 2017, the /16 (65,536 numbers) continued to be a popular block size for both large and mid-block buyers. For the first time, there were many blocks smaller than a /16 transferred as part of larger transactions.

Avenue4’s 2017 State of IPv4 Market Report – Analysis of the 2017 market and where it’s likely headed in 2018. (Download Report)In addition, large block buyers are more willing to accept smaller and smaller block sizes, which appeals to sellers that have substantial but fragmented unused address space. In 2017, the /16 (65,536 numbers) continued to be a popular block size for both large and mid-block buyers. For the first time, there were many blocks smaller than a /16 transferred as part of larger transactions.

We expect the small block market to continue to thrive over the next several years until IPv6 becomes the dominant Internet protocol. The large block market is another story, however. Although we expect additional large block supply to enter the market later this year into early 2019, mostly in the form of legacy /8 address space, the available large block space is dwindling and could disappear entirely within the next 2 years.

IPv6 migration was not a market factor in 2017.That should continue into 2018 and 2019 given the current pace of IPv6 adoption.

A full analysis of the IPv4 market, with additional data, can be found in Avenue4’s 2017 State of the Market Report.

Sponsored byDNIB.com

Sponsored byVerisign

Sponsored byVerisign

Sponsored byWhoisXML API

Sponsored byCSC

Sponsored byRadix

Sponsored byIPv4.Global

A World-Renowned Source for Internet Developments. Serving Since 2002.