Welcome:

Login

|

Sign Up

|

About CircleID

Follow:

|

|

|

|

||

|

||

At the end of June 2026, the share price of SpaceX is some USD $164 per share, and if you multiply that price by the total number of shares in the company, some 13.7 billion, you get a market capitalization of USD $2.163 trillion. The current estimate of the world’s population is 8.264 billion people, so the share price of SpaceX is currently at a phenomenal USD $261 per head.

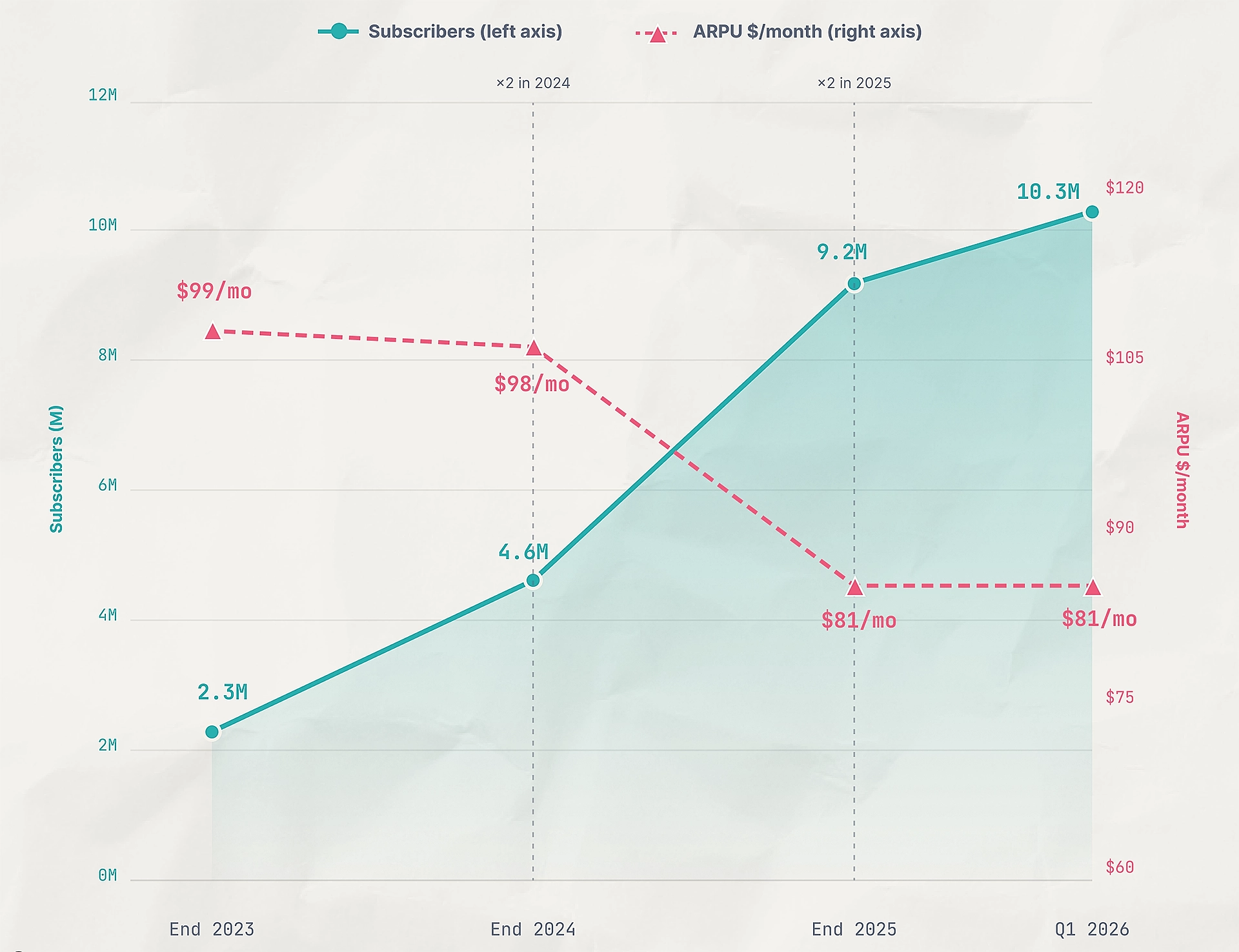

The average revenue per user (ARPU) for the Starlink business is some USD $66 per month, or USD $792 per year. That’s down from the 2023 reported ARPU of USD $1,188 due to international pricing in developing regions and a push to improve its market share in terrestrial markets. This company now has a market valuation of $261 per head of population but has a market penetration of just 0.0121% (Figure 1).

Even if Starlink increases its user base to a completely unlikely number of 1 billion users, each user will need to account for some USD $2,000 of value to justify the share valuation. At the same time, the ARPU of the global mobile industry sits between USD $72 and USD $120 per year, and it’s steadily declining over time at a rate of around 1.3% per annum. So, in ARPU terms, Starlink is outperforming the global mobile industry by an unsustainable factor of 8 or so.

But so far, Starlink is not a direct competitor to terrestrial mobile networks. Starlink can only do limited capacity services to mobiles, and falls far short of the 200Mbps–500Mbps of the terrestrial 5G networks. If you want to increase the capacity of the services offered to mobile devices, you need to use far larger antennae on the spacecraft, and the only provider (so far) in that particular market sector, AST Space Mobile, has demonstrated capacity up to 100Mbps by using spacecraft with antennae that fold out to the size of a tennis court! Starlink’s antennae in the spacecraft are far smaller, and when communicating with a mobile device with its unfocused antennae, the available channel capacity is invariably lower. In the mobile device space, equating Starlink services to today’s 5G terrestrial networks, Starlink looks like a triumph of exuberant hype over a more sobering reality.

The Starlink prospectus notes that: “Based on the total number of connected devices globally and the mobile ARPU, we estimate the Starlink Mobile market opportunity to be $740 billion.” Don’t forget that the current designs of the Starlink spacecraft do not use very large antennae, and the available capacity to service a mobile device is severely limited. It appears that a mobile device user is looking at a channel capacity of 4Mbps per second. Now, if you are one of the few individuals living in one of the far remote regions of the world, then anything, even this, looks good (although AST looks a whole lot better for direct-to-cell). But to get to the Starlink projection using an industry benchmark of USD $100 annual ARPU means that Starlink will need a significant user population of a billion or more, and with those numbers, Starlink is competing head-to-head with terrestrial mobile services with a substantially inferior service. This just doesn’t add up.

So perhaps this is all about the terrestrial broadband networks rather than mobile systems. The industry rate of broadband ARPU is approximately double the ARPU of mobiles, at some USD $240 per year.

Starlink has gathered some 10 million predominantly broadband users to date. SpaceX reported 2025 revenue of USD $18.67 billion. Connectivity services contributed USD $11.39 billion, or 61% of the total.

Here, Starlink’s prospects look healthier, in that an ARPU of some USD $1,000 per year is four times the industry benchmarks for fixed broadband. However, Starlink has been positioned so far with a user-terminal-based service that generally delivers between 50 Mbps and 250 Mbps downlink and 20Mbps–50Mbps uplink. Starlink V3 satellites are reported to have a total of 1Tbps of downlink capacity and 160Gbps of uplink capacity, divided into 48 individual down beams and 16 uplink beams. If you happen to be the only active Starlink user in a cell, it may be possible to have a 1Gbps downlink capacity. On the other hand, if you happen to live in an urban environment that is served with fiber cable infrastructure, current market offerings are edging towards capacities four times that capacity. A 50G-PON deployment splits a common 50Gbps capacity using a splitting ratio of between 1:32 and 1:64. So the market values such fixed broadband services at an ARPU of USD $240 per year. For a fixed broadband service, Starlink is offering an undistinguished access service, and where broadband is already available, Starlink needs to compete for market share on price alone. Starlink’s business edge lies in rural and remote areas, and here it’s far cheaper than a fixed fiber deployment. But rural and remote is by definition a very small part of the market, and if you want to grow your user base at some point, you are looking at the more densely populated and serviced areas of urban and suburban broadband connectivity. This analysis implies that the ARPU of a Starlink broadband access service in densely populated urban markets needs to be USD $200 per year or lower for a service with a capacity of up to a Gbps, which is a far lower number than Starlink’s current ARPU of USD $792 per year for a smaller capacity service.

Starlink’s prospects lean heavily on many more and much better future satellites. But there are some issues here. In the broadband access market, Starlink uses radio spectrum that has been dedicated to satellite communications, KU (10.7–12.7 GHz down and 14.0–14.5 GHz up) and KA-band (17.8–20.2 GHz down and 27.5–30.0 GHz up). Greater capacity is coming with V-Band ( 37.5–42.5 GHz down and 47.2–51.4 GHz up) and E-Band (71.0–76.0 GHz down and 81.0–86.0 GHz up).

In the mobile world, Starlink uses S-Band signals (1.9Ghz and 2.0Ghz). For mobiles, this direct-to-device satellite capacity may still be about one hundredth of the capacity per square kilometer of a 5G network operating in a sparsely populated rural environment. But Starlink is not saying that it will offer coverage only where there is no existing 5G service. It’s expected that it will compete in all locales, including not only rural and remote, but also urban and suburban. With an inferior service. And with expectations of a higher ARPU for this service.

So how could a satellite-first radio-based service become the preferred access service in the densely populated locales of suburbs and cities? The more mundane world of the intersection of utility economics and radio physics says “it can’t”.

In bidding up the share price to USD $160 and more, investors are not valuing SpaceX on the current service profile of Starlink as a connectivity utility operation. It is necessarily based on a hazy future of what SpaceX might become.

Alongside Starlink, the SpaceX prospectus talks up its prospects on X, Grok, payments and artificial intelligence. The company estimates a US$2.4 trillion market for AI infrastructure, a US$760 billion market for consumer AI subscriptions, a US$600 billion digital advertising market and points to a digital economy expected to reach US$22.7 trillion in the next couple of years.

Connectivity is not the business plan. In the eyes of SpaceX, connectivity is the customer acquisition strategy, and the value lies in the other activities that users will perform on these Starlink-connected devices, where presumably Starlink will be in a position to corral these users to SpaceX services and extract a far greater revenue sum from these activities. Starlink brings the customer on board. Mobile keeps them engaged. X captures attention. Grok becomes the AI assistant. X Money handles transactions. Enterprise AI tools generate recurring business revenue. In that world, connectivity becomes less important as a profit center and more important as a control point.

We’ve heard and seen all this before. In the telco world, the introduction of mobiles heralded the prospect of the mobile platforms where connectivity captured the customer, and the apps on the mobile device captured the user’s attention, payments, information tool and business device. The original, and very naive, view on the part of the telcos saw these apps as being managed by the mobile operator, and a small fraction of the revenues coming from this line of activity would fund a new golden age for the telcos. Obviously, this did not happen. Applications flourished, but outside of the overarching control of the connectivity provider.

We saw a similar play with Apple and its iPhone, and Google and the Android platform, where Apple and Google attempt to channel all mobile transactions through their respective stores, where they can take their share of the action. The problem is that many regulatory regimes want to see this sector of the market exposed to open competition, and the price of constantly defending a usurious and completely one-sided business model in every part of the world has created an environment where the only way that Apple and Google can relieve even a small part of this pressure is to reduce their fees. This attrition won’t relent until the entire capture model is destroyed.

So, the question behind this wild share valuation is: Will Starlink fare any differently in trying to leverage device connectivity into a position where it is taxing the transactions that occur with those devices?

Previous iterations from this exact same playbook say: Of course not!

What we are left with is a classic economic bubble.

Bubbles are fundamentally driven by speculative hype and exploit herd behavior, contradicting a financial commentary. Key drivers include:

Economist J. K. Galbraith viewed economic bubbles not as rational market anomalies, but as products of mass psychology and “financial euphoria.” He argued that speculative manias thrive on the illusion that there is “something new in the world”. Bubbles are driven by a growing disparity between an asset’s true economic value and its inflated price. Investors stop focusing on business fundamentals of markets, costs, profits, and dividends, and instead rely solely on the expectation that prices will climb forever, or at least long enough to make a substantial gain and sell the asset to a greater fool. Once a bubble bursts, it inevitably triggers intense periods of blame. Individuals who were widely regarded as financial geniuses during the boom are suddenly villainized. The rest of us switch to a position of sober sanctity, conveniently ignoring our own roles in the prior collective insanity.

So it’s time to strap in, as it’s going to be a fun ride!

Sponsored byDNIB.com

Sponsored byRadix

Sponsored byVerisign

Sponsored byIPv4.Global

Sponsored byWhoisXML API

Sponsored byCSC

Sponsored byVerisign

A World-Renowned Source for Internet Developments. Serving Since 2002.