Welcome:

Login

|

Sign Up

|

About CircleID

Follow:

|

|

|

|

||

|

||

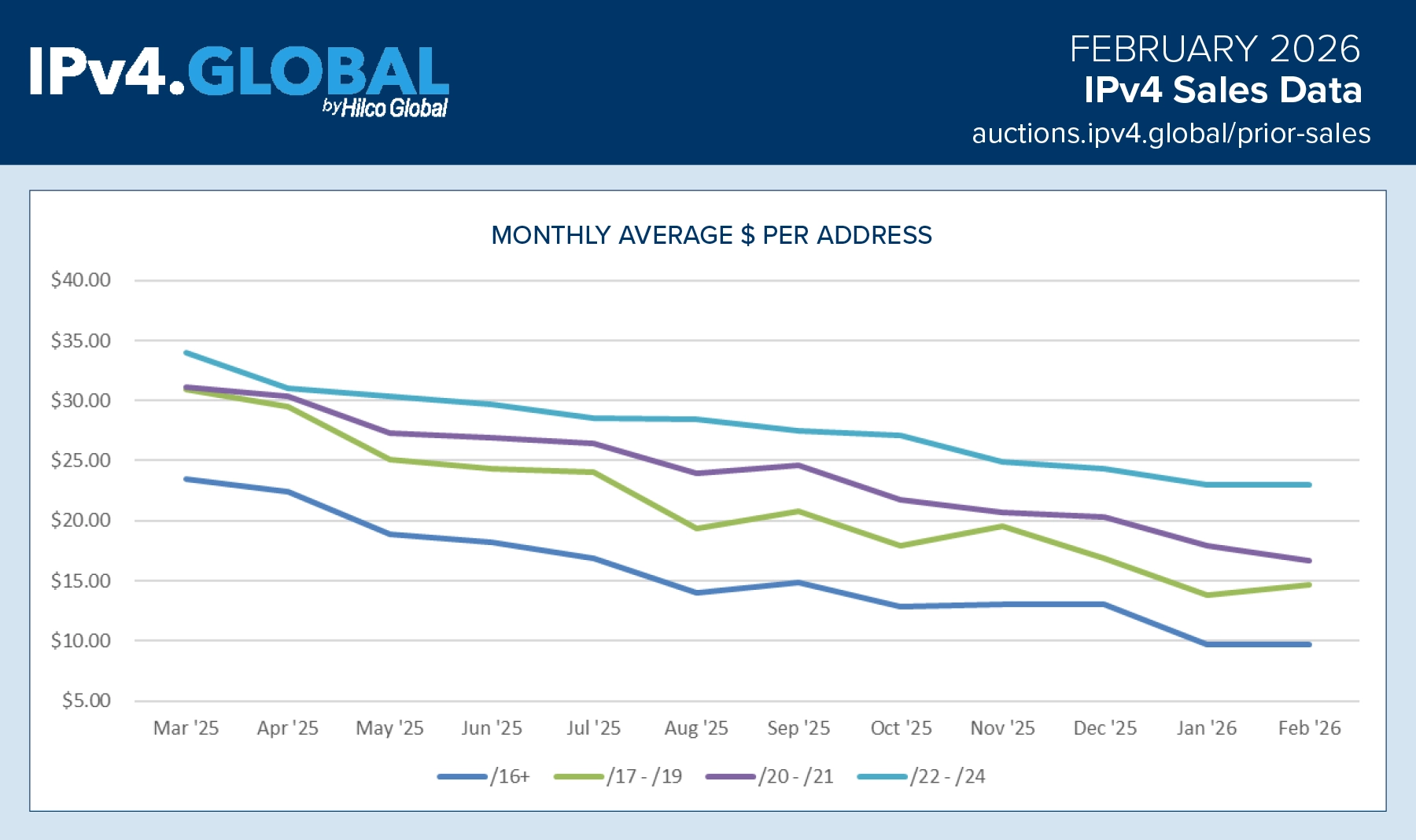

February 2026 finds the IPv4 market in a more mature phase: prices have continued to ease, yet transaction activity remains healthy and buyer participation broad. The chart supplied by IPv4.Global shows a clear downward trend across all block sizes through 2025, with the steepest absolute declines occurring in larger blocks and the most pronounced relative pressure visible in /16+ transactions. By February 2026, average /16+ pricing has fallen to just under $10 per address, down markedly from the low-$20s in March 2025, while mid-sized and smaller aggregates have also reset lower over the same period.

This correction appears less a sign of market weakness than of price discovery in a more liquid environment. As pricing has become more accessible, the pool of qualified buyers has widened beyond the most urgent acquirers. Network operators, cloud and hosting providers, intermediaries, and financially oriented buyers continue to participate, suggesting that demand for routable IPv4 space remains structurally intact even as pricing power has softened. In practical terms, lower prices have improved market clearing, encouraged transaction velocity, and supported a steadier flow of negotiated transfers.

That resilience matters. A declining price curve would ordinarily imply deteriorating fundamentals. In IPv4, however, the opposite may be true: broader participation, deeper liquidity, and continued deal execution point to a market that is functioning efficiently rather than retreating. Buyers still need address space for growth, migration timing remains uneven, and IPv6 adoption, while advancing, has not displaced near-term operational demand for IPv4.

The data, however, require careful reading. Reported sales include both online and private transactions; some blocks may form part of larger bundled agreements with negotiated pricing; and prices are recorded at agreement date rather than transfer date. These factors can introduce timing effects and dispersion around monthly averages.

The outlook entering 2026 is therefore measured but constructive. Further pricing softness remains possible, especially in large blocks, yet market depth and transaction health suggest an orderly market, not a distressed one.

Sponsored byDNIB.com

Sponsored byIPv4.Global

Sponsored byWhoisXML API

Sponsored byVerisign

Sponsored byVerisign

Sponsored byCSC

Sponsored byRadix

A World-Renowned Source for Internet Developments. Serving Since 2002.