Welcome:

Login

|

Sign Up

|

About CircleID

Follow:

|

|

|

|

||

|

||

IPv4.Global’s April 2026 market report highlights steady pricing, resilient demand, and broader transaction activity as signs the IPv4 transfer market may be entering a more stable phase.

The IPv4 transfer market entered the second quarter of 2026 with an unusual combination of softer historical pricing, firmer transaction activity, and increasingly broad-based demand. After nearly two years of gradual price compression, recent market data suggests the sector may be moving into a more constructive phase—one characterized less by speculative retrenchment and more by operational buying.

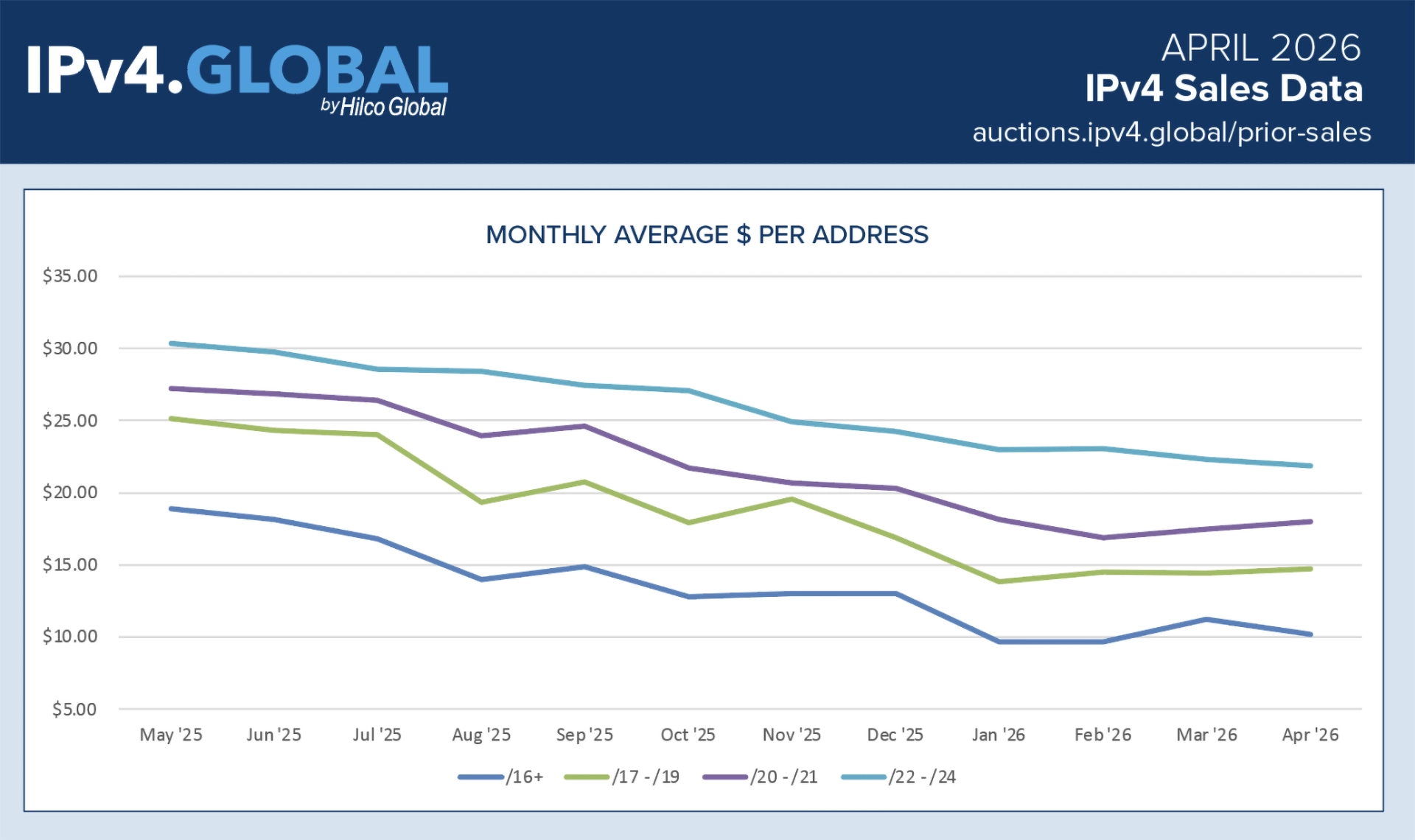

April’s pricing data reinforces that narrative. Across all major block sizes, average prices per address remained broadly stable following stronger activity in March. The accompanying sales chart illustrates the longer trajectory clearly: values have declined materially since mid-2025, but the pace of deterioration has slowed considerably in recent months. Larger, cleaner blocks continue to command the highest premiums, while smaller allocations remain more price-sensitive. Still, even the most affected segments showed signs of stabilization through April.

The /22 – /24 category, historically the market’s premium tier due to routing efficiency and deployability, averaged just above $21 per address in April, down from roughly $30 a year earlier. Mid-sized blocks (/20 – /21) settled near $18, while /17 – /19 ranges remained in the mid-$14 territory. Larger aggregated holdings (/16+) continued to trade near $10 per address. The important development, however, is not merely where prices sit, but how they are behaving. The steep downward repricing seen through much of 2025 has given way to flatter month-to-month movement and steadier bid activity.

That pattern aligns with broader industry observations emerging across the address-transfer ecosystem. Recent market commentary has pointed to a shift in buyer composition. Opportunistic and financially motivated participants appear less dominant than during the market’s peak pricing era. In their place are enterprise operators, hosting providers, cloud infrastructure firms, and regional networks purchasing address space to meet immediate operational requirements. Such buyers tend to be less sensitive to short-term market timing and more focused on deployment certainty, registry compliance, and acquisition efficiency.

Several structural forces continue to underpin this resilience. IPv6 adoption, while steadily advancing, remains uneven across enterprise environments, consumer hardware, and software ecosystems. Many organizations continue to operate dual-stack networks or maintain IPv4-dependent services for compatibility reasons. Meanwhile, AI infrastructure growth, edge deployments, and emerging-market broadband expansion continue to absorb IPv4 resources despite ongoing efficiency improvements.

Regional diversification has also become more pronounced. Transaction activity in early 2026 was not concentrated in a single geography or block class, suggesting healthier underlying market participation than headline pricing alone might imply. This breadth matters. Markets nearing exhaustion often narrow toward only premium inventory; today’s activity suggests buyers remain active across multiple categories.

For buyers, the current environment may represent one of the more favorable acquisition windows of the past several years. Pricing remains well below historical highs, yet recent trading patterns imply the market may have passed its cyclical low. For sellers, conditions are improving incrementally. While valuations remain disciplined, liquidity and transaction confidence appear materially stronger than they were even six months ago. Organizations holding surplus or underused address space may find this an opportune time to sell unused inventory, particularly before a broader market recovery strengthens pricing and reduces buyer flexibility.

The outlook for the remainder of 2026 is cautiously constructive. A rapid return to prior peak pricing appears unlikely absent a major supply shock. Nevertheless, if demand continues at current levels and pricing stability persists through the middle of the year, the IPv4 market may transition from a prolonged correction into a period of measured recovery.

Sponsored byVerisign

Sponsored byVerisign

Sponsored byCSC

Sponsored byWhoisXML API

Sponsored byIPv4.Global

Sponsored byRadix

Sponsored byDNIB.com

A World-Renowned Source for Internet Developments. Serving Since 2002.