Welcome:

Login

|

Sign Up

|

About CircleID

Follow:

|

|

|

|

||

A wave of high-profile cyberattacks is reshaping the global insurance industry, creating both risk and reward for major players. According to a new Bloomberg report, firms like Munich Re and Chubb are capitalising on surging demand for cyber insurance as artificial intelligence makes digital breaches more frequent and destructive.

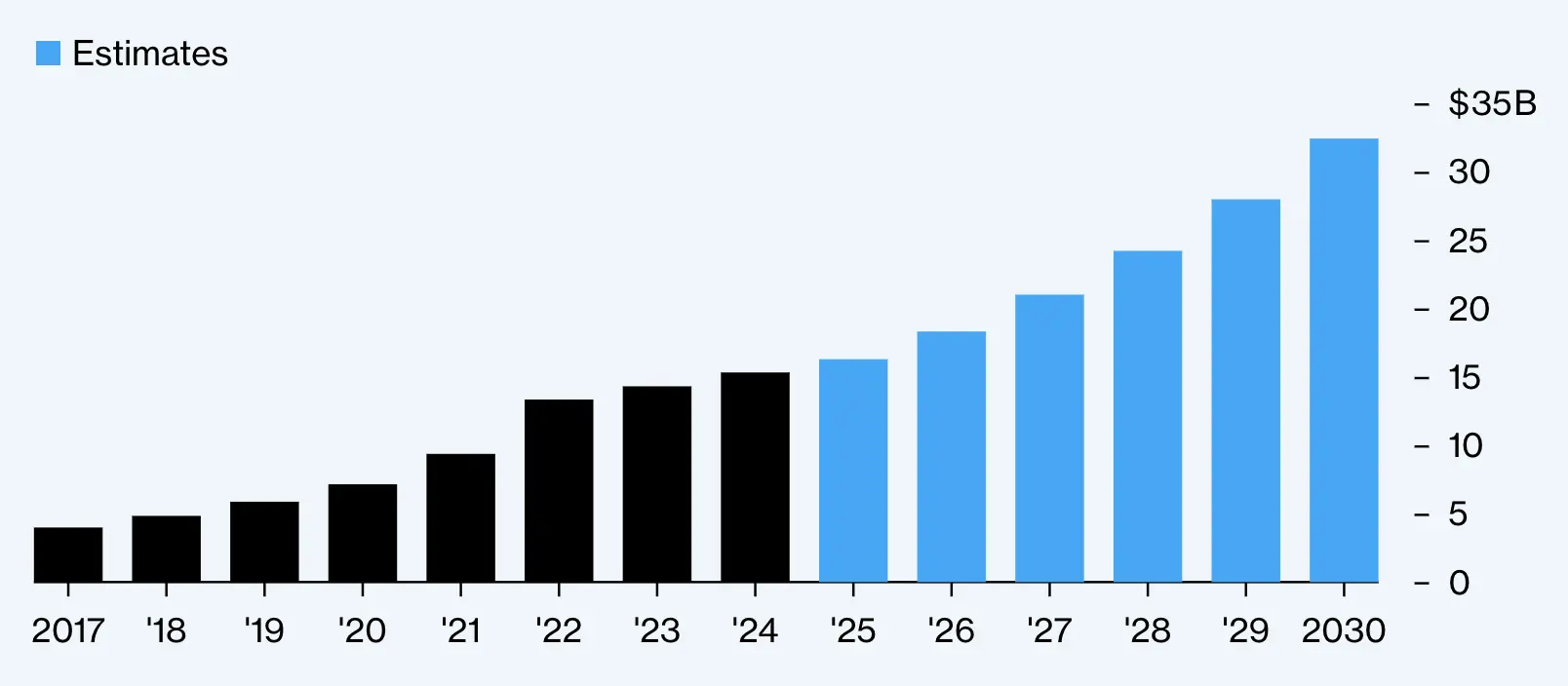

Market projections: The cyber insurance market is projected to reach $16.3 billion in 2025, rising to $30 billion by 2030. Despite this growth, a vast swathe of global digital risk remains uninsured. Losses from cybercrime soared to $9.5 trillion in 2024, up sharply from $600 billion in 2018.

Massive financial losses: The recent hack on Marks & Spencer, which could cost the retailer £300 million in operating profit, has jolted the market. Demand for coverage surged immediately after the breach, said Sydonie Williams of Beazley, a key insurer in the sector. “There was a sense of ‘that could have been us,’” she noted.

Coverage gaps: Such incidents are triggering a broader reassessment of insurance coverage and pricing. Analysts suggest that claims of this magnitude may not immediately raise premiums, but will likely fuel an upward trajectory. Insurers are expected to tighten policy terms or increase prices to reflect elevated risk.

Still, uptake remains limited. Fewer than half of FTSE 100 firms have cyber policies, and coverage among smaller businesses is even sparser. With recession fears looming, affordability could dampen further investment. Nevertheless, firms investing in internal cybersecurity are helping to reduce risk and premiums, creating what analysts describe as a “virtuous cycle.”

Sponsored byVerisign

Sponsored byDNIB.com

Sponsored byCSC

Sponsored byRadix

Sponsored byIPv4.Global

Sponsored byWhoisXML API

Sponsored byVerisign

A World-Renowned Source for Internet Developments. Serving Since 2002.