Welcome:

Login

|

Sign Up

|

About CircleID

Follow:

|

|

|

|

||

|

||

IPv4.Global sees stabilization across block sizes through 2026 with renewed buyer demand, tightening supply expectations, and AI infrastructure growth pointing toward a more favorable environment for sellers.

Good predictions are good guesses made by experienced market observers. At IPv4.Global, the world’s largest IPv4 marketplace and the most comprehensive source of secondary market pricing data, we consider ourselves unusually well-exposed to the forces that move this market. The data we have collected across many thousands of transactions, combined with observable supply and demand dynamics across every major RIR region, gives us a reasonable basis for projecting what buyers and sellers should expect for various block size ranges through the end of 2026 and into 2027. These are our best-informed assessments, not guarantees, but not guesses made in the dark either.

The story of the past two years is one of dramatic divergence, a market correction that arrived faster and fell further than most observers predicted, and now, cautiously but clearly, the early signs of a new phase. Understanding that arc is essential context for any forward-looking view.

To predict where prices are going, it is worth establishing precisely where they have been.

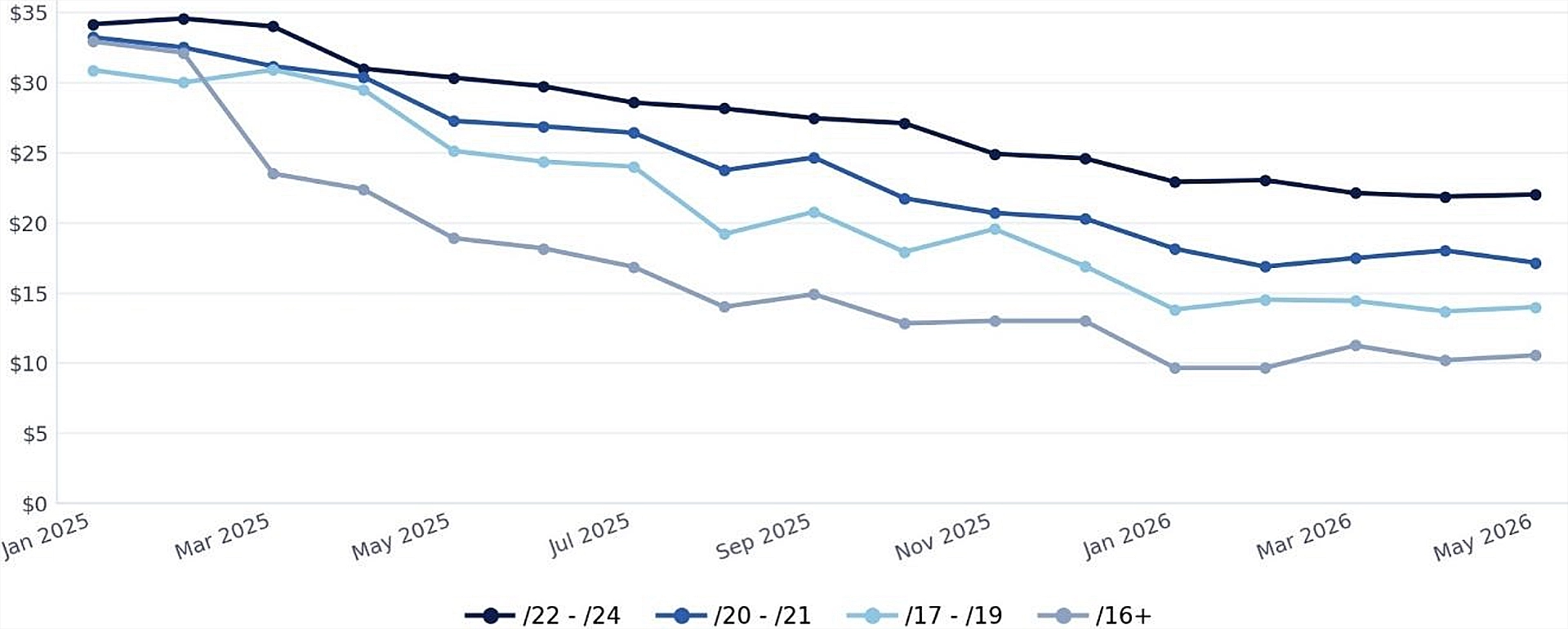

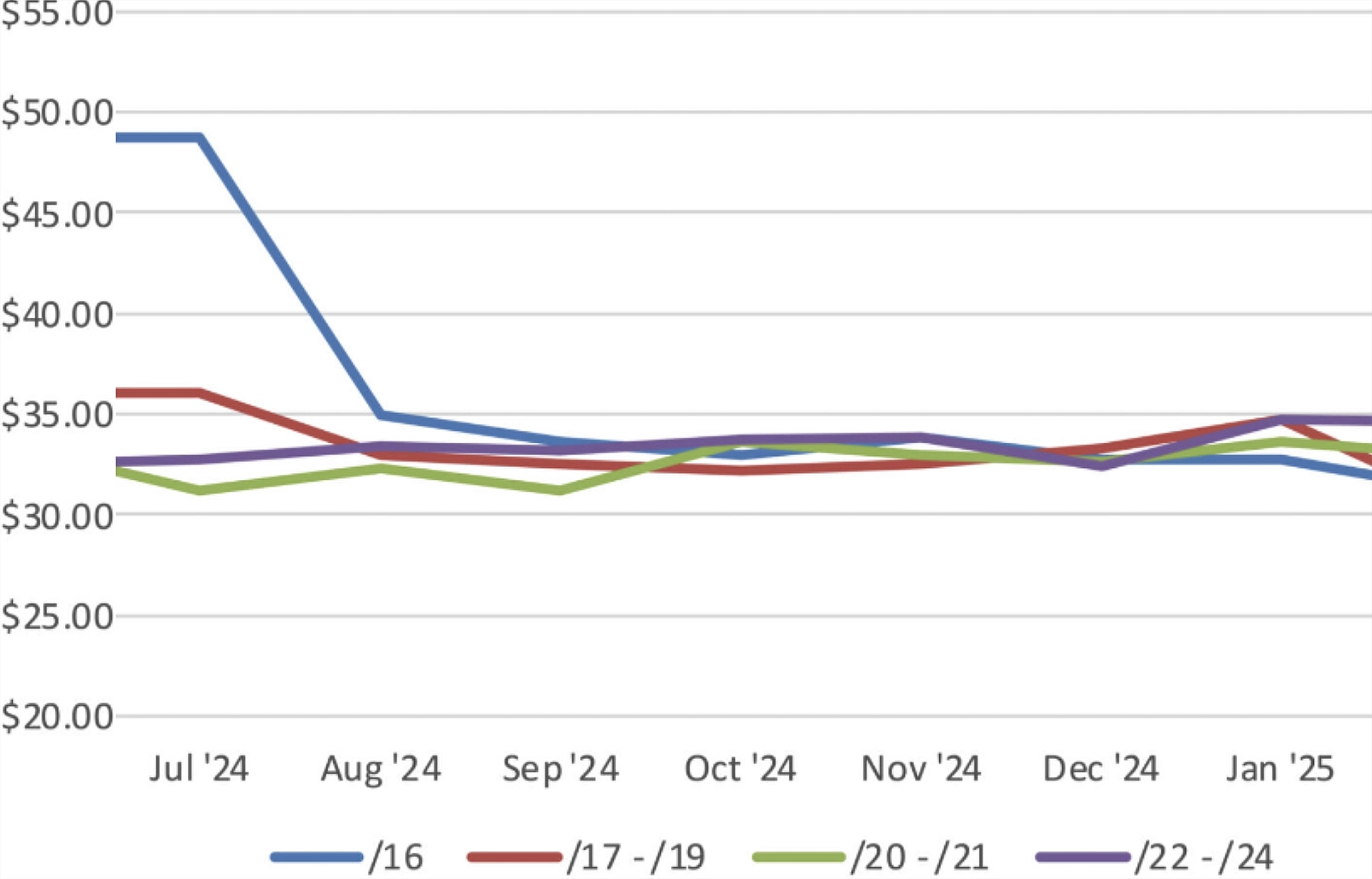

In late 2023, the IPv4.Global marketplace reported per-address pricing for /16 and larger blocks hovering near $52 per address, while smaller blocks in the /20-/24 range were changing hands at roughly $36. The premium commanded by large blocks was historically anomalous, a 44% spread between large and small blocks on a per-address basis. The cause of this pricing divergence was well understood by most observers: hyperscale cloud operators were accumulating large contiguous address inventories for infrastructure expansion. Their demand for intact large blocks drove pricing to levels that could not persist once that demand cycle ended.

That high level of demand persisted until July 2024. The correction was swift and steep. “Convergence” was anticipated but the cause not predicted. During the second half of the year all block sizes traded hands at approximately the same $33 per address.

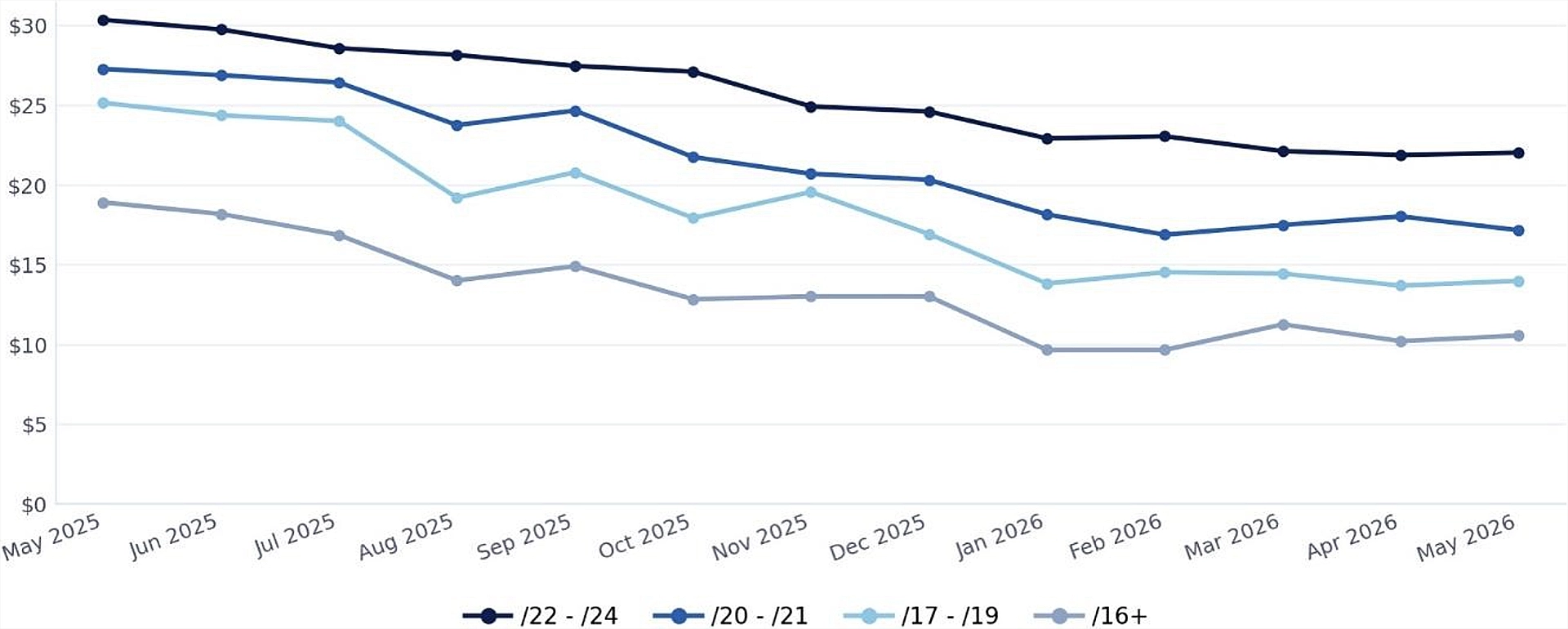

After a period of improvement, prices began to pull back in early 2025 before drift slightly apart. Blocks began trading at small but significantly different price ranges relative to one another. By May 2025, the /16 crossed below $20 per address for the first time since 2019, a threshold that served as a vivid marker of how far the correction had run. The decline did not stop there. Through the balance of 2025, /16 blocks began the year near $33 per address and fell below $13 by the fourth quarter, a contraction of more than 60% over the course of a single year.

Mid-size blocks followed their own trajectory. Blocks in the /17-/19 and /20-/21 range experienced similar downward pricing pressure, ending 2025 closer to $16 and $21 per address, respectively. Smaller blocks, /22 through /24, showed more resilience. While not immune to the broader pricing environment, they declined more modestly, ending the year in a range that still represented a meaningful premium over larger blocks. The trend that once favored large blocks evened out, then fully reversed: By mid-2025, small blocks were priced at more than twice the per-address rate of /16s in some transactions.

Throughout all of this, something important did not break: demand. Transaction volume remained strong. The pool of active buyers increased meaningfully across 2025, powered in large part by investment in AI infrastructure, diversifying to include cloud-native firms, regional ISPs, digital infrastructure startups, and enterprises pursuing strategic acquisitions for long-term operational use rather than speculative resale. The number of transactions recorded at IPv4.Global’s marketplace in July 2025, 98 for the month, was 32% above the monthly average of 73, even as prices were declining. This decoupling of price from volume is the most important structural signal in the 2025 data: the market was not contracting; it was repricing to a new equilibrium.

The first four months of 2026 showed a clear shift in the trend.

January 2026 saw transaction volume reach new highs and a notable influx of new buyers entering the space. Prices for large blocks continued downward in January, reflecting the completion of larger package transactions at negotiated rates, but the buyer pool expansion was itself a leading indicator. February brought the first real question from market observers: had we seen the floor? Pricing appeared to hold, even inching upward for some block sizes, as demand continued strengthening. March delivered the clearest signal yet, a measurable price uptick across the market, with volume and demand described as strong and diverse across both industry verticals and geographic regions.

April 2026 confirmed that March was not a statistical artifact. Pricing remained stable, demand was broad across block sizes rather than concentrated in any single segment, and the directional signal remained cautiously positive.

It is worth being precise about what this means and what it does not. A few months of stabilization and modest uptick do not constitute a recovery to 2022 peak pricing. Prices remain well below historical highs across every block size category. But the direction has shifted. The question is no longer whether prices will continue falling indefinitely. The question is the shape and pace of the recovery, and that is a materially different question to be asking.

Before projecting forward, it is useful to anchor the analysis in what the data shows across the major block size categories as of late 2025 and early 2026.

These experienced the most dramatic correction in 2025, a decline of more than 60% from the beginning to the end of the year, with /16 blocks falling from roughly $33 per address in early 2025 to below $13 by Q4. Some multi-package block transactions cleared below $10 per address in late 2025 and early 2026. By any historical measure, these were 10-year pricing lows. The driver was a combination of persistent supply, legacy holders, universities, telecoms, and restructured organizations monetizing underutilized assets, and the near-complete withdrawal from brokered markets of hyperscale cloud buyers who had been the dominant demand source for large, contiguous blocks.

These occupied an intermediate position, declining in parallel with large blocks but at a somewhat reduced rate. /17-/19 blocks ended 2025 near $16 per address; /20-/21 blocks ended near $21. The compression between large and medium block pricing narrowed the gap that had historically made medium blocks a preferred acquisition for organizations unable to absorb a full /16.

These were the relative anchors of the 2025 market. While not immune to the broader pricing environment, smaller blocks showed more modest declines. They were supported by a buyer base that is structurally broad and operationally driven. Small ISPs, hosting providers, and enterprises needing targeted address space for specific applications form a persistent, recurring buyer pool. The ongoing incentive for businesses to purchase addresses and bring them to cloud platforms via BYOIP programs also disproportionately supports small block demand. Pricing for /22-/24 blocks ended 2025 at a meaningful premium to larger blocks, though some convergence with medium block pricing began in the latter part of the year.

The data from the first four months of 2026 points to a market that has likely found a floor and that is beginning the process of recovery. Here is what we expect for each block size category through the end of 2026.

Recovery Has Begun, but Pace Matters

Large blocks are coming off their most compressed pricing levels in a decade. The conditions that produced the decline, hyperscale withdrawal, elevated legacy supply, and downward price expectations, have not all reversed, but they have moderated. Supply is less frenzied than it was at the height of the 2024-2025 sell cycle. Sellers who have not yet entered the market are watching the stabilization signals and may be less eager to undercut now that the floor appears visible.

For the remainder of 2026, we expect /16+ pricing to recover gradually from the $10-$13 per address range seen in late 2025, moving toward a band of $15-$22 per address by year-end. The upper end of that range is more likely if hyperscale buyers, or the AI infrastructure operators who represent the emerging equivalent, re-enter the market meaningfully. It is worth noting that AI workloads and GPU cluster deployments require substantial IPv4 space for management networks, API endpoints, and customer-facing services. This represents a category of demand that did not exist at scale during the 2020-2021 large-block buying cycle and could accelerate recovery beyond current expectations.

Transaction prices will continue to vary by region and by deal structure. ARIN-registered space has historically commanded a 5-15% premium over RIPE throughout market cycles, and that is unlikely to change. Package deals and negotiated private sales may continue to clear toward the lower end of market ranges regardless of published pricing trends.

Convergence and Partial Recovery

Medium blocks are the most dynamic pricing category in the current environment. Having compressed toward large-block pricing during 2025, they are positioned to recover as large-block prices stabilize and begin moving upward. At the same time, buyers who found /16s too large or operationally unwieldy may increasingly find /17s and /18s attractive at relatively modest premiums over /16 pricing.

We expect /17-/19 blocks to trade in the $18-$26 range per address by late 2026, and /20-/21 blocks to be in the $22-$30 range. This represents meaningful recovery from 2025 lows but still reflects a market where large and medium block pricing has compressed significantly relative to the 2022-2023 spread. The variance on medium block transactions has historically been high, and pricing will likely continue to scatter across a significant range, making current market data and transaction-level comparables more valuable than any published average.

Stable, with Modest Upward Pressure

Small blocks remain the most liquid and consistently priced segment of the market. The buyer base is broad, distributed, and operationally driven. This produces consistent demand regardless of what is happening at the large-block end. The April 2026 observation that demand was broad across multiple block sizes rather than concentrated in one segment is a positive indicator for this category.

For the remainder of 2026, we expect /22-/24 pricing to hold in the $28-$40 range per address, with ARIN-registered space continuing to command a premium. If the broader market recovery continues, small-block pricing could inch upward as buyers who have been deferring purchases accept current levels as near-bottom. A range of $30-$36 per address represents the most probable outcome for transactions through year-end 2026, with ARIN blocks toward the higher end.

The structural tailwinds for small blocks remain intact. AWS, Azure, and their peers charging for IPv4 address allocation on their platforms creates ongoing incentive for businesses to purchase addresses in the secondary market and bring them to the cloud via BYOIP programs. That demand is price-sensitive but structural, it does not go away as long as cloud providers charge for IPv4 usage. Additionally, leasing rates for small blocks have remained remarkably stable throughout the purchase-price correction, hovering in a $0.38-$0.50 per IP per month range across most RIPE and ARIN blocks. The persistence of lease rates above equivalent sale-price yields creates a floor for purchase prices at the small-block end of the market that does not exist in the same way for large blocks.

The IPv4 secondary market has completed one of its most dramatic repricing cycles on record. Large blocks fell more than 60% from early-2025 levels to their late-year lows. Small blocks held comparatively firm, producing a spread between large and small block pricing that was historically extreme and operationally significant for anyone thinking about buy-sell strategy. As of mid-2026, the market appears to have found its floor, and the early data suggests a measured recovery is underway.

For 2026, we expect large blocks to recover gradually from current levels, reaching $15-$22 per address by year-end; medium blocks to trade in the $18-$30 range depending on size; and small blocks to hold firm in the $28-$40 range with modest upward pressure. For 2027, the base case is continued gradual convergence, a market that looks more like its long-run equilibrium than the extremes of either 2022 or late 2025, with a 30-50% premium for small blocks over large blocks. The upside scenario, driven by AI infrastructure demand or hyperscale re-entry, could accelerate that recovery meaningfully.

Markets repeat themselves. This one has moved through cycles of divergence and convergence more than once, and the current cycle is no exception. Those who read the data clearly and act on it tend to fare better than those who wait for certainty the market is never going to provide.

Pricing data and market commentary are drawn from IPv4.Global Marketplace. IPv4.Global’s third-party analysis published by CircleID, IPXO, i.Lease, and independent market observers. Historical pricing data is available at the Marketplace. This analysis represents market observations and informed projections, not investment or legal advice. Individual transaction prices vary materially based on block size, registry, reputation history, and negotiation.

A Message from Our Sponsor

How to Take Advantage of Rising IPv4 Address Value: IPv4.Global specializes in helping clients sell, lease and buy IPv4. We help make the process less complicated and time-consuming by:

• Helping you find a buyer

• Leading you through the registry process

• Providing advice and expertise to reorganize your network

Contact us by calling (212) 610-5601 to speak with an expert for help turning your invisible asset into revenue.

Sponsored byVerisign

Sponsored byWhoisXML API

Sponsored byRadix

Sponsored byCSC

Sponsored byVerisign

Sponsored byIPv4.Global

Sponsored byDNIB.com

A World-Renowned Source for Internet Developments. Serving Since 2002.