Welcome:

Login

|

Sign Up

|

About CircleID

Follow:

|

|

|

|

||

|

||

Every ICANN-accredited registrar signs the same Registrar Accreditation Agreement. The obligations that follow from it, including data retention, RDAP provision, transfer handling, and abuse reporting, apply identically whether a registrar manages 61 million domains or none at all. This uniformity is a deliberate design choice. It ensures predictability, equal treatment, and a level playing field, and it has served the DNS well for over two decades.

What has been missing from discussions about this model is a systematic measurement of the market it governs. Concentration among a small number of large operators is widely assumed in the industry. But assumptions are not measurements, and until recently, nobody had quantified the structure of the gTLD registrar market at the level of individual operators using ICANN’s own public data.

I have now done that measurement, and the results were published in IEEE Access this month. This article summarizes what the data show.

ICANN publishes monthly registry transaction reports for every gTLD, listing per-registrar counts of additions, renewals, transfers, deletions, and restores. I collected these reports for eight of the largest gTLDs (.com, .net, .org, .info, .shop, .store, .top, and .xyz) over 24 months, from January 2023 to December 2024. Together, these TLDs accounted for roughly 87 percent of all gTLD registrations as of Q1 2025.

One methodological step matters for interpreting the results. Many operators hold multiple IANA accreditations. Treating each accreditation as a separate registrar would fragment the picture, so I grouped accreditations that share an operational base, identified through contact domains and naming conventions, into single registrar entities. After this consolidation, the dataset covers 676 registrar entities and 69,131 registrar-TLD-month records.

The entire pipeline, from raw ICANN CSVs to the final analysis tables, is written in Python and [openly available on Zenodo](https://doi.org/10.5281/zenodo.15619901) under an MIT license. Anyone can re-run it, check it, or extend it.

Three findings stand out.

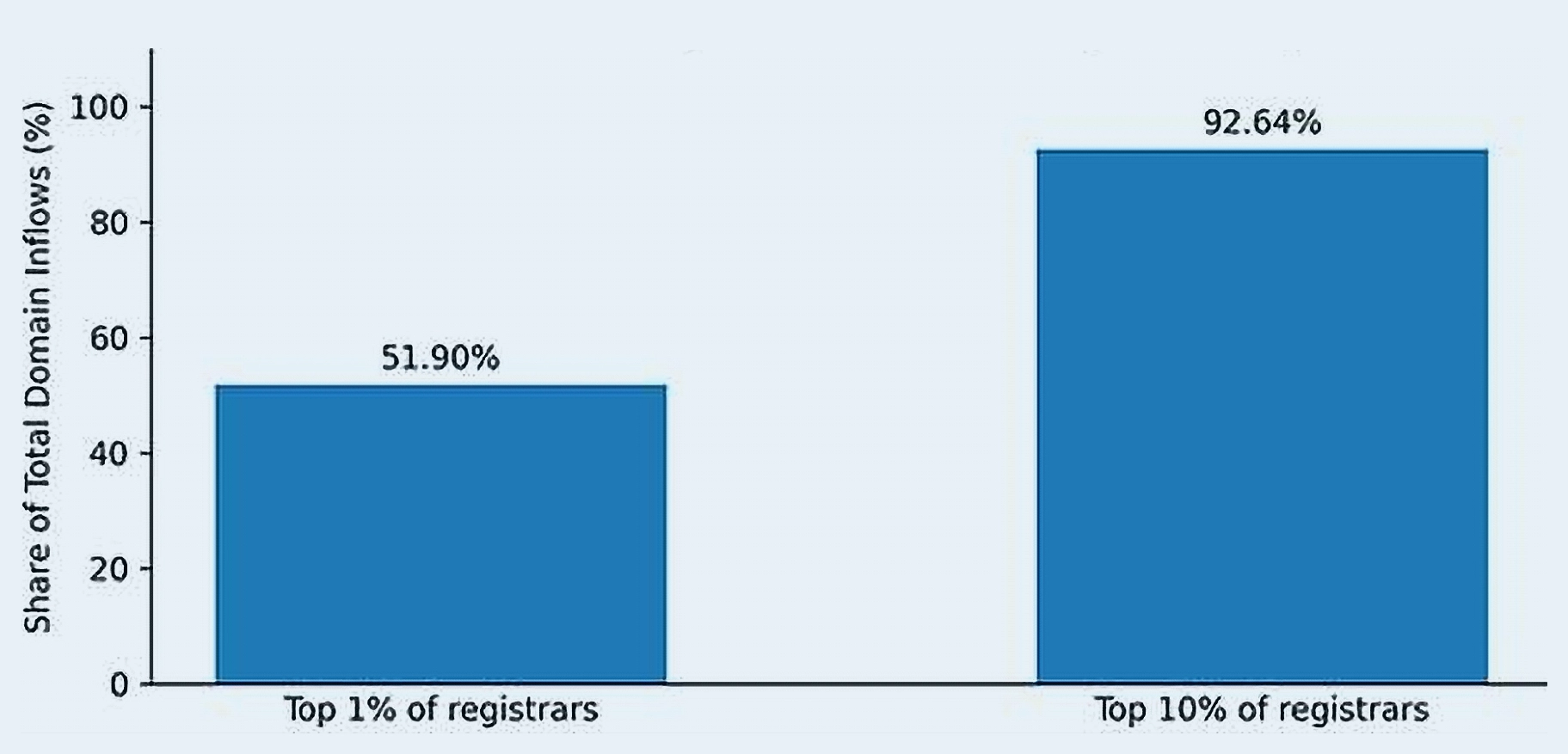

First, the degree of concentration was, at least to me, surprising. The top 1 percent of registrar entities, which is seven companies, account for 51.9 percent of all inflows, defined as new registrations plus incoming transfers. The top 10 percent account for 92.64 percent. The bottom half of all accredited registrars together contribute 0.028 percent. The Gini coefficient for inflow activity is 0.94. This is not specific to any single TLD: when measured separately, each of the eight gTLDs shows a Gini coefficient above 0.93, legacy and new alike.

Second, a substantial long tail of accreditations is essentially dormant. Using a conservative threshold of fewer than ten inflows and ten outflows across the entire two-year window, 116 entities, about 17 percent of the sample, recorded almost no transactional activity at all. Their portfolios persist through renewals, but their contribution to market dynamics is negligible.

Third, renewals dominate everything. Nearly half of all recorded transactions, 49.7 percent, are renewals. For most registrars, renewals exceed all other transaction types combined. The gTLD registrar business, as reflected in transaction data, is primarily a portfolio maintenance business, with new market activity concentrated among a small set of large operators.

A regional pattern is worth noting. EU-domiciled registrars are measurably less concentrated than the rest of the market: the top 10 percent of EU entities account for 72.9 percent of EU inflows, compared to 94.9 percent for non-EU entities. Part of this difference likely reflects a thicker middle of medium-sized European operators. Part of it may simply reflect that European registrars conduct much of their business in ccTLDs, which are invisible in gTLD transaction reports. The data cannot separate these explanations.

Two limitations deserve emphasis, because they define what conclusions the numbers can and cannot support.

Reseller networks are invisible. ICANN’s reports show the accredited registrar of record. A wholesale registrar appears as a single entity, even though its volume is distributed across thousands of resellers. The retail-level market is therefore likely less concentrated than these figures suggest. The accreditation-level market, however, is exactly as measured, and since ICANN’s contractual obligations attach at the accreditation level, that is the relevant level for questions about the contractual framework.

The analysis is descriptive, not causal. It quantifies structure. It does not explain why the market looks this way, nor does it test whether any particular policy change would improve anything.

The policy context makes the measurement relevant. European regulation has moved decisively toward proportionality: the GDPR, the DSA, and NIS2 all scale obligations to an entity’s size, risk, or impact. ICANN’s contractual framework, with one narrow exception, does not. That exception is the Registrar Data Escrow program, in which registrars with more than 100,000 registration years per quarter face more frequent deposit obligations. Scale already determines obligations in this one instance.

Whether that principle should extend further is a policy question, and it is not one this study answers. Reasonable people in the ICANN community disagree about proportionality, and the uniform model has genuine virtues that any differentiated approach would need to preserve. What the study contributes is the empirical baseline that has been missing from the discussion: a reproducible, verifiable picture of how uneven the market actually is. The rules apply equally to seven companies that handle half of all new business and to 116 accreditations that handle none essentially. Whatever position one takes on what follows from that, the number itself is now on the table.

The paper, “A Data-Driven Analysis of Structural Asymmetries in the gTLD Registrar Market,” is open access in IEEE Access (doi: 10.1109/ACCESS.2026.3709387). The dataset and analysis pipeline are on Zenodo (doi: 10.5281/zenodo.15619901).

Sponsored byCSC

Sponsored byRadix

Sponsored byWhoisXML API

Sponsored byIPv4.Global

Sponsored byVerisign

Sponsored byDNIB.com

Sponsored byVerisign

A World-Renowned Source for Internet Developments. Serving Since 2002.